Bet_Noire

Above: The FY saw sharp increases in revenue, AEBITDA across every one of the verticals in the LNW portfolio.

The trail from Scientific Games to Light & Wonder

We go way back with Light & Wonder, Inc. (NASDAQ:LNW) stock, though we have not covered it since 2022 (Hold rating) because of its lapse into a bad business model. We now resume coverage because the company has been transformed into a tightly managed, innovative leader in the gaming equipment and systems space. We expect continuing earnings beats ahead.

We begin in the early 1980s when I had created the first-ever industry publication covering the entire spectrum of legal gambling in casinos, gaming equipment, horse racing, lotteries, and monitoring systems.

One of our early Gaming Business advertisers was a company called Scientific Games, which specialized in the creation, production, and distribution of scratch-off games for state lotteries. The two partners visited our headquarters in New York as part of a marketing launch for their latest cards that featured gambling icons.

They were also planning an IPO at the time just as the industry was going through a major growth cycle. But what stayed with us past the days of that visit was the conviction that their long-term plan was to expand beyond lotteries to the entire gambling ecosphere.

We bought the stock at the low did well and sold it after it had merged with legacy slot machine maker Bally Manufacturing Corp in 2014.

Then, as the years passed, we observed the exponential growth of the company, eventually spanning all those verticals they’d promised. The problem was that by 2021 they had clearly overshot the mark. Their hot pursuit by investment and merger or acquisition brought the company deeper in debt. Their original clear vision had become blurred and confused. By the early 2020s, they were in real trouble both with their core lottery business as well as their foray into sports betting.

The choices ahead were clear: Either consolidate and trim down the company, or risk financial troubles beyond their capacity to deal with them. They had in fact a situation similar in many ways to that of Walt Disney today. They had expanded into too many businesses, taken on too much debt. The answer to their ills had to be massive slashing of their ambitions and tight focus on building a profitable core.

So, they sold their lottery and sports betting businesses. The stock became far easier to understand for investors. And the concentrated effort on its remaining verticals has paid off.

lnw archives

Above: Supercharged growth in online casino mobile games.

In 2022, the company name was changed to Light & Wonder (LNW) to focus on three verticals: gaming machines and revenue sharing slot systems, IGaming and the Sci Play social platform gaming business. They paid $22.95 a share. The full acquisition was completed by Q4 2023.

That leads us to now. They have accomplished their goals, and Mr. Market is showing up as a believer.

Above: Despite being below the radar screen, smart money has found LNW.

LNW today: It’s a strong buy after a strong FY23 performance

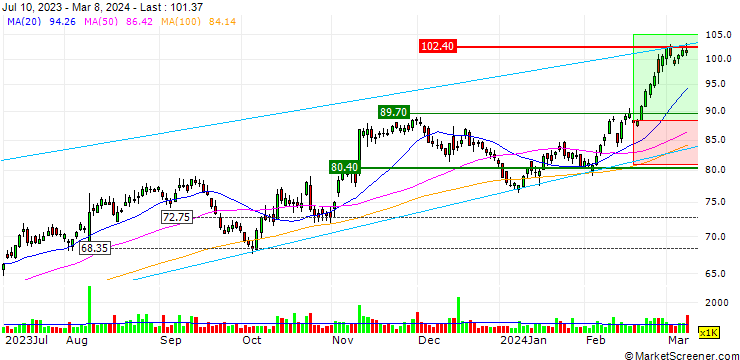

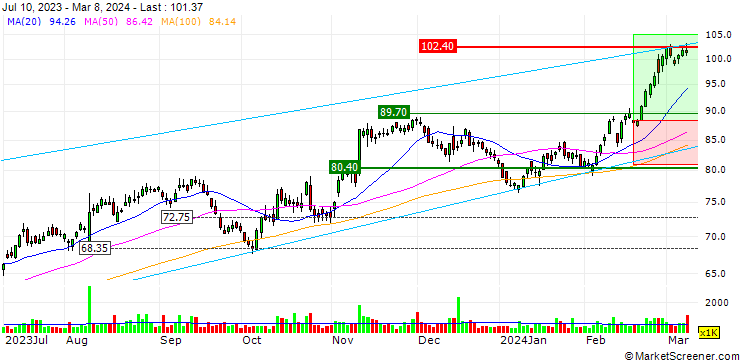

LNW: Price at writing $99

FY 2023 top line results

- 11 consecutive quarters of revenue growth. Revenue up 13% y/y. Stock repurchases for the year $170m.

Results by segments:

- Gaming (machine sales and revenue sharing casino slot revenue for installed base) $490m up 31% y/y.

- SciPlay: Online social gaming platforms $204m up 12%.

iGaming (online casinos) $70m up 16% y/y.

lnw archives

Above: LNW capacity to continually adding new games keeps revenue moving.

- Installed base of slot share machines at casinos was up 7%.

- Gaming division AEBITDA $245m up 12%.

- Debt: $3.9b. Despite cash outlay to complete merger of SciPlay, LNW repaid a term loan last month saving 35bps or $8m in interest cost going forward.

- Cash on hand: $425m.

- Total revenue FY23: $2.9b.

Investment return model

To illustrate Mr. Market’s response to LNW trending, this investment return model is clear:

- One year with a buy in at $10,000 end value $15,700.

- Starting price per share (1 year ago) $62.29.

- End price at writing: $101.83.

- Compound annual return: 61.74%.

- AEBITDA margin: 39%.

- FCF $291m.

Conclusion

Our strong buy guidance here is rooted in the old poker player’s admonition made famous by the Kenny Rogers hit, You gotta know when to hold ‘em and know when to fold ‘em.

In my view, this adage expresses one of the best characteristics of a smart corporate management: Moving to recognize and cut your losses and then rebuild your business model to reflect realities in the markets in which you operate.

In the case of LNW, a restructured management team went hammer and tong at the accumulated problems that led it into vast over expansion. They came out at the other end with a solid, cross-platform gaming equipment, systems and online operator with a great future. Right now Statistica has the value in USD of $500b globally spent on all forms of legal gambling. It projects a CAGR of 5.7%, which would put the industry at USD$800b by 2030.

This reflects both growth in existing markets plus the ignition of legalization in new markets. That growth includes brick and mortar casinos planned or in the process of development, online betting sites and a migration of social gaming site customers to real money wagering. What this all means is that companies like LNW will participate in this growth cycle through all its verticals going forward.

To meet this demand, Las Vegas based LNW develops new games every year to address market demand adapted by region. This includes U.S., Asia, Oceana, and the EU, where they currently have a sales presence.

The margin of safety, we believe, comes from the tracking of the stock over a year we have noted above. It is not like some sports-betting platforms that tend to trade in spurts up or down based on investor overreaction either way to quarterly or event-driven data suggesting a powerful surge in betting action, or a slowdown. By contrast, our research on the trading patterns of LNW indicates its trading pattern is more closely allied to quarterly results or the release of new games that attain great popularity.

For those reasons, we are putting a price target of $135 on Light & Wonder, Inc. shares by the results of Q2 or early Q3 this year.